BY FAZAAD BACCHUS

In our last issue we discussed that the Government of Canada had put measures in place to assist with the financial stress of COVID-19.

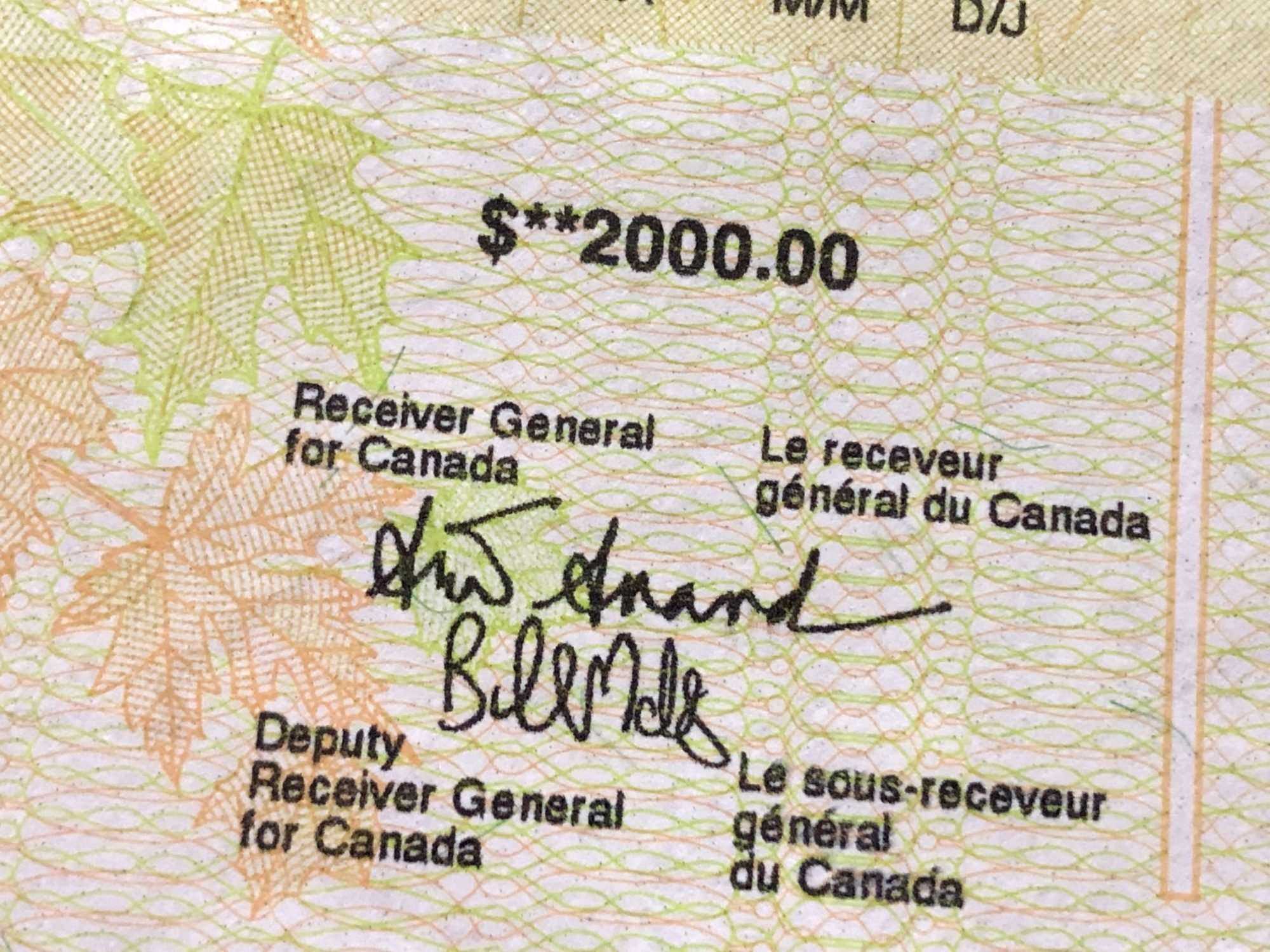

This benefit is available to workers residing in Canada, who are at least fifteen years old and have stopped working because of COVID-19 and have not voluntarily quit their job or are eligible for EI regular or sickness benefits. You had income of at least $5,000 in 2019 or in the 12 months prior to the date of their application and are/or expect to be without employment or self-employment income for at least fourteen consecutive days in the initial four-week period. Since the last issue there has been a new development where if you expect to earn less than $1,000 per month, you can apply also for the CERB benefit.

Let us focus on the taxes payable on this CERB income. The first thing to note is that this benefit is taxable, however there is no deduction at source. This means that taxes on the total amount you receive must be paid when you file your taxes in 2021 – in respect of your total 2020 income. Everyone will have their own marginal tax rate (which is based the highest dollar earned in 2020) and it will be used to determine the amount of taxes due on the CERB. To better explain this, I will provide you with two examples.

Harry earned a total of $3,000 between January and February this year and then was laid off due to COVID-19. He applied for the CERB and received a benefit of $2,000 per month for four months amounting to $8,000. Harry did not work again for the rest of the year and therefore his total income was $11,000. On this amount of total income, Harry does not have to pay any taxes on his CERB, the reason being his total income is below the tax threshold and may even qualify for a refund for taxes withheld on the first $3,000.

Shanti on the other hand earns $3,500 per month and earned a total of $7,000 between January and February and was also laid off due to COVID-19. Like Harry she applied and received a benefit of $8,000 over the four months. However, Shanti goes back out to work (if all goes well) in July and earns her normal salary of $3,500 per month. Shanti would have earned a total of $28,000 in regular income plus $8,000 in CERB and an amount of $36,000. In this case she must pay back approximately $1,600 in taxes on the CERB and it is payable when taxes are filed next year.

This amount is magnified with individuals who are in the highest tax bracket who may have to pay back as much as $4,320. Therefore, it is recommended that you put aside a part of this money to cater for taxes next year. Another way to alleviate this problem is to make a RRSP contribution to reduce your taxes.

Stay in the loop with exclusive news, stories, and insights—delivered straight to your inbox. No fluff, just real content that matters. Sign up today!