Transferring money abroad consistently creates a problem for those looking to transfer their funds from Canada. There are so many questions to consider, and a wide range of fees or exchange rates that need to play a factor, as well. Many people who are looking to transfer their money abroad consider two primary channels for doing so: a currency provider or a bank. It’s tough to know which of these channels is the best for money transferring. Luckily, we’ve done the legwork for you and researched a few of the most popular currency provider and bank for money transferrers from Canada. Let’s take a closer look.

The Benefits of Bank Transfers

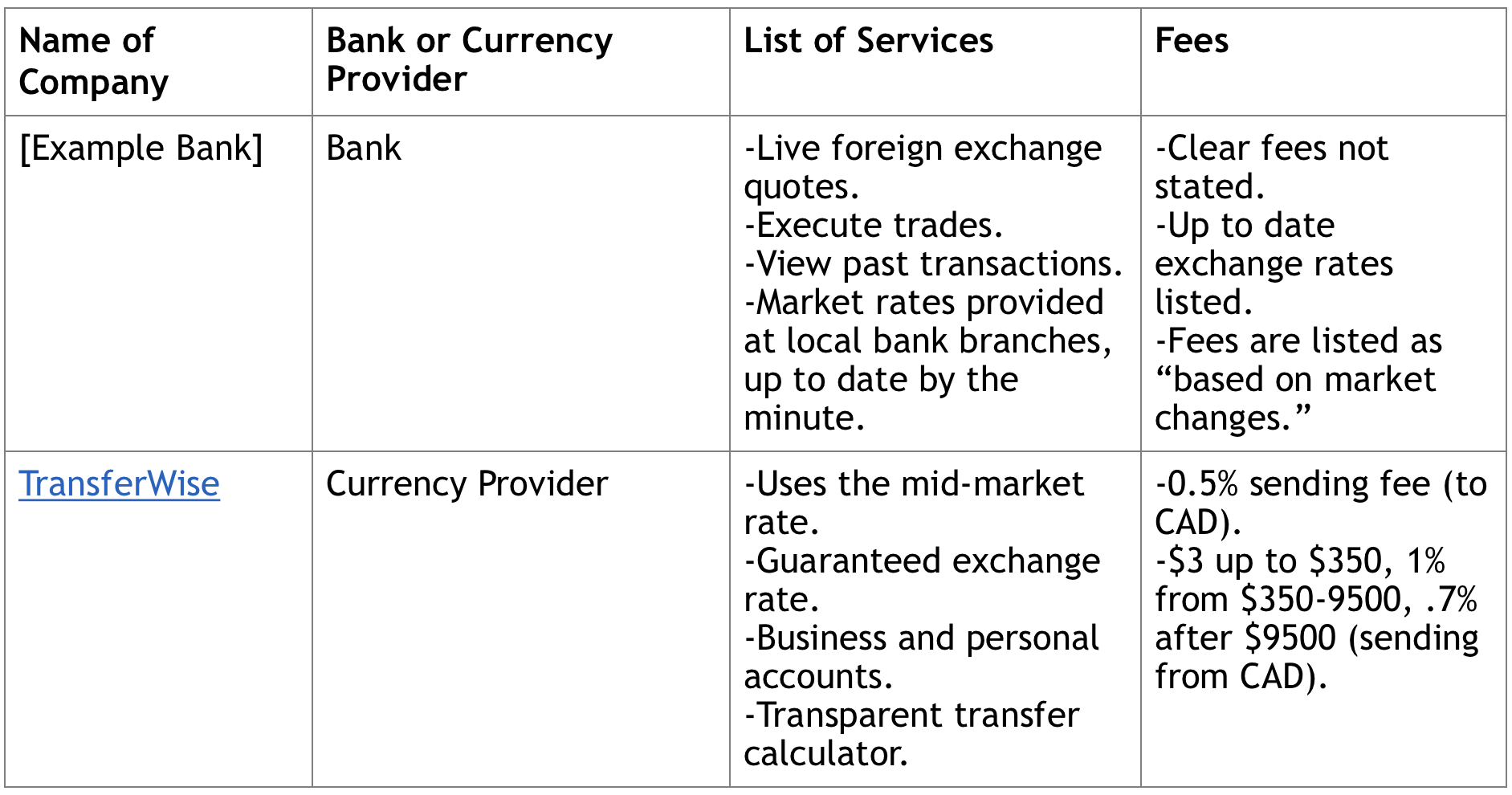

Many people prefer bank transfers because they’re simply what we know. In general, if you have an account with a bank, you might feel more comfortable transferring money abroad using them. They have direct access to your account and, in theory, should be looking out for your best interest. Banks also provide an up to date list of exchange rates either on their websites or when you contact your local brick and mortar bank location. Many of them offer foreign exchange services online, which is also convenient.

The Negatives of Bank Transfers

There are a few glaring negatives to transferring money using a Canadian bank. The most prominent downside can be seen in the comparison table above – there is no clear statement of fees. While you may be able to call your local chapter of the bank you have an account with to get a list of these fees, the fact that they aren’t transparently states on their site raises concern. Admittedly, the transfer rates are listed clearly on most banking websites, but there’s still a question of what you’ll pay in fees per transfer, depending on the amount of funds you’re transferring. If we look at our example bank, as we did in the comparison table above, it’s also clear that they don’t go out of their way to make these foreign exchange transfers easy for their account holders. You must sign up online, there is no available transfer calculator, and the site’s content clearly states that fees and rates are subject to change at any time. There is no guarantee that’s clearly stated.

The Benefits of Currency Providers

Transferring money from Canada with currency providers, such as TransferWise, has a lot of benefits. The biggest benefit is that all fees are made very clear on the currency providers’ website. They even provide an easy-to-use calculator that shows what fees you’ll be paying along with the most up to date median market rate you’ll be getting for your transfer. TransferWise also guarantees any transfer rate if they receive funds from you within 24 hours. Most currency provider companies have a similar guarantee.

The Negatives of Currency Providers

Currency providers are a new organization concept, and most of them are online-only. While they do have readily accessible customer service and support teams to assist you if necessary, they don’t have brick-and-mortar locations you can visit and have a face-to-face interaction with a representative should you have questions. For most people, this isn’t a negative. In fact, younger generations of money transferrers would prefer to not leave the comfort of their home to complete a transfer. However, if you crave that brick-and-mortar location, currency providers won’t be able to provide that for you.

In Summary

While currency providers and Canadian banks both get the job done when it comes to foreign exchange services, currency providers will come out on top with lower transfer fees and the best available exchange rates in almost every situation. While there are some benefits to completing foreign exchange transfers with your local bank they’re too minimal to truly outweigh the benefits that a currency provider, like TransferWise, brings to the table. Banks often don’t clearly list their transfer fees, and it’s because they change regularly and are usually high. Currency providers, on the other hand, are known for clearly stating their fees upfront. The only true “win” that Canadian banks have over currency providers in the money transfer realm is their availability of brick-and-mortar locations for patrons to visit and complete their transfer – and that’s hardly enough to make their high (or unlisted) fees worth it.

Stay in the loop with exclusive news, stories, and insights—delivered straight to your inbox. No fluff, just real content that matters. Sign up today!